The Unspoken Loophole: Why Lenders Don’t Sign Mortgages

Before getting started, please subscribe to our 𝕏 account at https://x.com/ParalegalsToday

Introduction

When a borrower takes out a mortgage, they assume they are signing a fully enforceable contract. After all, their signature is required on every document. But what if the mortgage itself—the security instrument that allows the lender to foreclose—is missing a key element? The lender’s signature.

While the Promissory Note is a clear contractual obligation for repayment, the Mortgage or Deed of Trust often lacks full execution by the lender. This loophole creates serious legal implications for enforcement, securitization, and borrower rights. In this article, we’ll break down the issue, examine relevant case law, and provide a comprehensive checklist for paralegals, mortgage professionals, and borrowers.

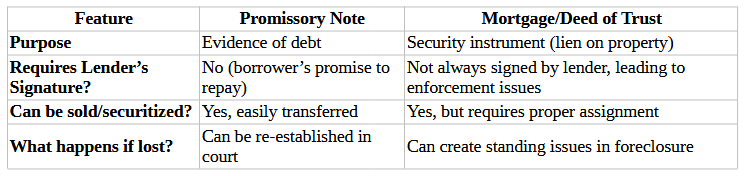

The Promissory Note vs. The Mortgage: Key Distinctions

Key Legal Issues When Lenders Don’t Sign

Lack of Mutual Assent: A contract requires agreement by both parties—but if the lender never signs, did they ever formally accept the terms?

Enforceability of Foreclosure: Can a lender enforce a mortgage in court if they never executed it?

Assignment & Securitization Problems: If the mortgage is transferred, but the original lender never signed, does the new holder have legal standing?

State Law Variations: Some states require lender signatures; others allow enforcement based on conduct and payments.

Case Law on the Issue

Secrest v. Security National Mortgage Loan Trust 2002-2, 167 Cal.App.4th 544, 546 (Cal. Ct. App. 2008) – Held that a Forbearance Agreement/modification agreement without the lender’s signature was unenforceable under the Statute of Frauds. (The Forbearance Agreement constitutes a modification of the note and deed of trust.)

Chavez v. Indymac Mortgage Services, 219 Cal.App.4th 1052, 1055 (Cal. Ct. App. 2013) – Ruled that a lender could be equitably estopped from denying an unsigned modification agreement.

Carpenter v. Longan (1872) – Established that the note and mortgage must remain together for enforcement, raising issues when improperly assigned.

Some legal principles and related cases provide insight into this issue:

Statute of Frauds: This legal doctrine requires certain contracts, including those involving real estate, to be in writing to be enforceable. Typically, the borrower's signature suffices to meet this requirement, as the borrower is the party to be charged.

Promissory Note and Mortgage Distinction: The promissory note, signed by the borrower, represents the debt obligation. The mortgage or deed of trust secures this obligation with the property as collateral. Courts often consider the note and mortgage together, focusing on the borrower's commitment.

Case Law on Related Issues:

Eaton v. Federal National Mortgage Association (2012): The Massachusetts Supreme Judicial Court held that a foreclosing mortgagee must also hold the promissory note at the time of foreclosure. While this case doesn't address lender signatures on mortgages, it emphasizes the importance of the lender's relationship to the note and mortgage.

Landmark National Bank v. Kesler (2009): The Kansas Supreme Court ruled that all indispensable parties must be identified in foreclosure actions, highlighting the necessity of clarity in mortgage documentation. This case underscores the importance of proper documentation but does not specifically address the lender's signature on the mortgage itself.

The prevailing legal framework suggests that the borrower's signed promissory note and mortgage are typically sufficient for enforcement. However, ensuring that all parties properly execute mortgage documents is a best practice to avoid potential legal disputes.

Why Lenders Don’t Sign Mortgages: A Historical and Legal Perspective

The Real Reason Lenders Don’t Sign Mortgages

Lenders avoid signing mortgages for control, flexibility, and legal advantage. By keeping their signature off the document, they:

Ensure unilateral borrower obligation – The mortgage is enforceable against the borrower alone.

Make securitization easier – Mortgages can be freely assigned and sold without additional contract complications.

Avoid contractual defenses – If they don’t sign, they can argue they never "accepted" certain terms that could limit their rights.

It’s all about retaining power while shifting risk entirely onto the borrower.

The Historical Reality: Lenders Once Did Sign

In the early days of banking, mortgages were treated as true bilateral contracts, requiring both borrower and lender signatures to demonstrate mutual assent. This was in line with traditional contract law principles, where both parties had to agree in writing for enforceability.

However, as the financial industry evolved, lenders pushed for a unilateral structure to facilitate:

Easier enforcement – No lender signature means fewer borrower defenses.

Seamless secondary market sales – Investors prefer “clean” instruments without lender obligations.

Regulatory and liability avoidance – Signing could expose lenders to claims of bad faith or contractual breaches.

Wrap-up

The modern mortgage is a one-sided agreement by design. While mutual assent was once the norm, lenders deliberately abandoned signing mortgages to strengthen their legal standing, simplify transactions, and protect their interests. This historical shift highlights how financial institutions shape the law to their advantage—often at the borrower’s expense.

Mortgage Signing & Enforceability Checklist

I. Understanding the Lender’s Absence from the Mortgage Signature Line

Recognize the One-Sided Nature: Typically, the borrower signs the mortgage, while the lender does not.

Identify the Legal Justification: Courts often enforce mortgages based on the borrower's assent, even without the lender's signature.

Understand the Benefits to Lenders: Not signing allows for easier enforcement, securitization, and transferability.

Consider Secondary Market Impact: Mortgage-backed securities (MBS) require easily assignable instruments, reducing lender liability.

Evaluate Risks to Borrowers: The absence of a lender's signature may limit borrower defenses in foreclosure proceedings.

II. Historical Context: Did Lenders Once Sign?

Examine Older Mortgage Documents: Historically, lender signatures were common, reflecting mutual assent principles.

Understand the Shift in Banking Practices: The evolution of financial markets led to the standardization of unsigned lender documents.

Assess State-Specific Requirements: Some states may still mandate lender signatures for certain documents.

Consider Early Banking Regulations: The transition from bilateral to unilateral mortgage contracts coincided with industry changes.

III. Legal Challenges & Borrower Defenses

Question Mutual Assent: Without a lender's signature, the traditional notion of a contract may be challenged.

Review State Laws: Certain jurisdictions may have specific requirements or interpretations regarding unsigned mortgages.

Analyze Conduct & Payments: Courts may consider the behavior of both parties in determining enforceability.

Identify Potential Borrower Defenses: Arguments may include fraud, lack of consideration, or improper securitization.

Consider Case Law:

Brown v. Allied Home Mortgage Capital Corp.: Highlighted that the absence of a lender's signature could render an agreement unenforceable, especially if the signature was a condition precedent.

Federal Home Loan Mortgage Corp. v. Guntzviller: Emphasized that a mortgage could be deemed void without the necessary signatures, particularly in cases involving co-owners.

IV. Key Documents & Lender Signature Requirements

Mortgage / Deed of Trust: Typically signed only by the borrower; however, state laws may vary.

Modification Agreements: Often require signatures from both parties to be enforceable.

Forbearance Agreements: Generally necessitate mutual consent through signatures.

Assignments of Mortgage: Lender signatures are essential when transferring the loan to another entity.

Satisfaction & Release of Mortgage: Lender signatures are required upon full repayment to clear the lien.

V. Best Practices for Professionals & Borrowers

Paralegals & Junior Attorneys: Stay informed about case law and enforceability issues related to mortgage documents.

Mortgage Professionals & Loan Closers: Ensure all legally required signatures are obtained to prevent future disputes.

Signing Agents & Notaries: Be vigilant about state-specific requirements for lender signatures and advise parties accordingly.

Borrowers & Homeowners: Thoroughly review all mortgage documents and seek legal counsel if uncertainties arise.

Litigators & Consumer Advocates: Explore lender non-signature arguments in foreclosure defense strategies, considering recent case law.

This comprehensive checklist integrates pertinent case law and offers actionable insights for various stakeholders involved in the mortgage process.

Conclusion: A Simple Fix for a Big Problem

The easiest way to avoid these legal battles? Lenders should sign mortgages, deeds of trust, and modifications. There is no legitimate reason for them to avoid executing a document that they expect to be enforceable against borrowers. By ensuring full execution, the legal system would eliminate ambiguity, reduce unnecessary litigation, and create fairness in the lending process.

For paralegals, attorneys, mortgage professionals, and borrowers, awareness is key. If a mortgage is missing a lender’s signature, it may not be as airtight as lenders claim. Always review loan documents carefully—because what isn’t signed can sometimes be just as important as what is.